Zero Based Budget Example: What We Did to Get Out of Debt

As an Amazon Associate I earn from qualifying purchases. For more details, please see our disclosure policy.

There are many approaches to paying down debt and gaining financial independence. Bryan and I paid off our debts in 2009. It took 18 months to pay off $18,000 in consumer debt. Here’s our zero based budget example that got us there.

Want to save this post?

Enter your email below and get it sent straight to your inbox. Plus, I’ll send you time- and money-saving tips every week!

You hear the word budget all the time: budget-friendly this, budget-friendly that. I think people often mean: “being frugal” when they say “budget”. But that’s not the same as having a budget.

A budget is a plan for how you will spend your money. It’s simply figuring out what you can spend on the different areas of your life without spending more than you have.

A zero based budget is a specific plan for spending your money, one that accounts for every penny, saved or spent down to zero. This is what we used to budget when learned what it is to live within your means and have continued the practice for debt-free living.

When we first got married, we were told by whom I have no idea, but I bet they’ve been talking to you, too. They told us to spend a certain % on housing and a certain % on food.

Well, those people certainly don’t live in Southern California. A flat thirty percent of one’s income doesn’t begin to cover the housing costs here.

For years it seemed like no type of budget clicked for us until we learned about the zero based budget example.

For years we struggled to create a workable budget since our income fluctuated with my husband being self-employed. We found out how to budget while self-employed people, tweaking other systems to fit our life and income.

The zero based budget was one of those systems we tweaked.

What is zero based budgeting?

If you make $5000 in a month, then you budget all the $5000. It’s that simple. One podcaster back in the day called it, “giving every dollar a name.”

That worked for us.

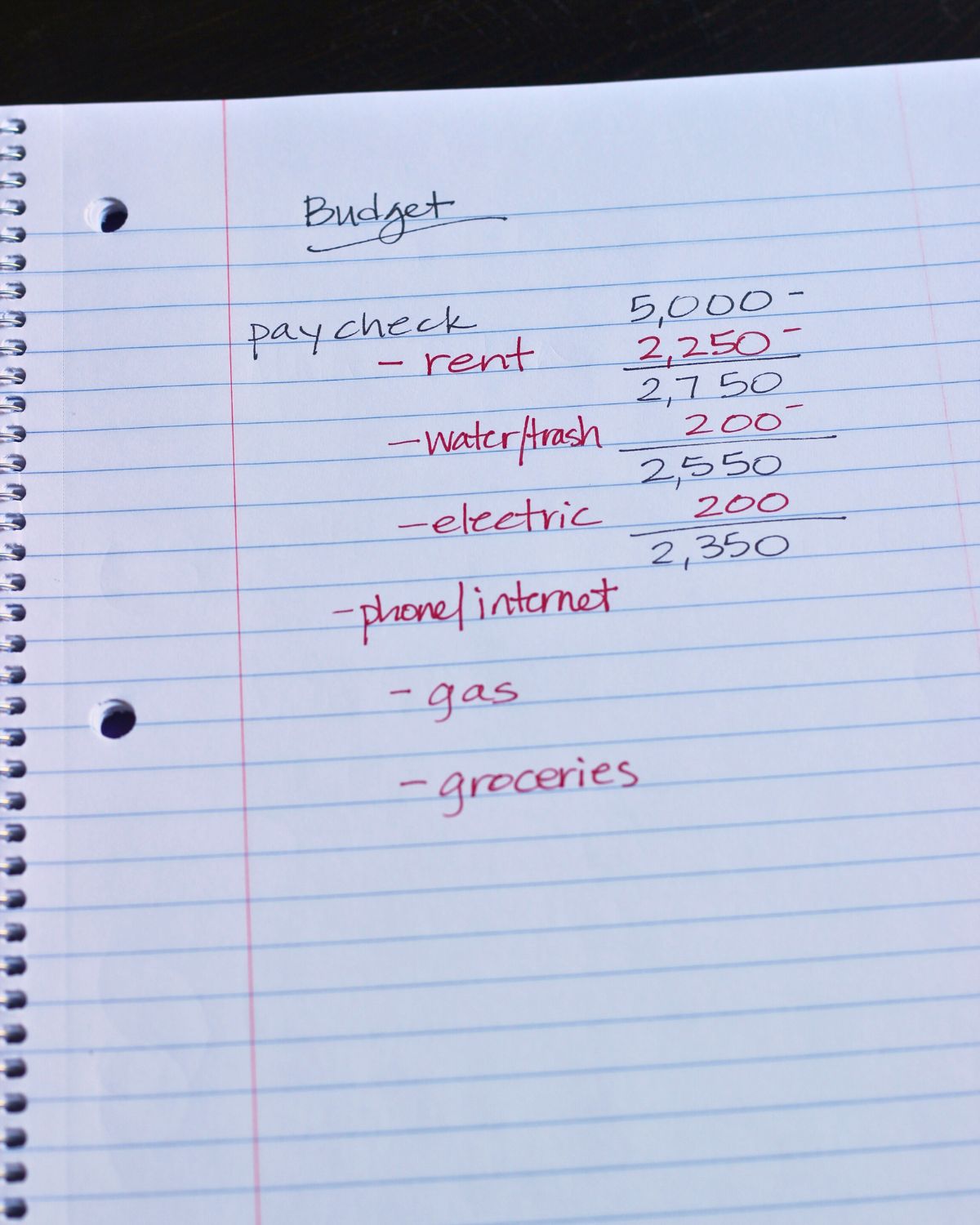

While there are apps that will do the math for you, I find that writing it down with pen and paper is my vibe. Here’s what our budget has looked like in the past:

And yes, it’s not uncommon for housing to cost 50% or more of your paycheck where we live!

How to Create a Zero Based Budget

Here’s our process for creating a zero based budget:

1. Determine your income.

Add up all your sources of income and identify that amount.

For us, we focus on the two regular checks we get each month: my husband’s paycheck and an inheritance he receives from his mom’s pension. That is our number to live on.

Any other income that comes in is being saved, earmarked to go into retirement or other sinking funds.

2. Figure out your baseline expenses.

Write a list of all your regular monthly expenses. You can use this Monthly Costs Worksheet if you’re doing this manually. It is a great tool to communicate things to your spouse during money meetings.

Communicating the amount of each bill in black and white is great. When we do this, I know my comments aren’t falling on deaf ears and he can see it clearly.

3. Subtract expenses from income.

Dave Ramsey uses this phrase a lot when coaching folks on budgeting: Give every dollar a name. It basically means that you’re going to determine what each dollar is for — before you spend it, if possible.

Take your income and start subtracting the expenses. If you do this line by line, then you really see how the money is “disappearing” as you spend it.

4. Make a plan for creative spending.

If you come up short or don’t feel enough comfort at the end of all that subtraction, you’re going to need to get creative.

- What can you do without this month?

- What subscriptions can you cancel?

- Do you really need to have cable, lunches out, or that new pair of shoes?

In seasons when we’ve needed to tighten up our spending, we brainstorm ideas to keep to our zero based budget. Here are some of the strategies we’ve used in the past:

- using cash to track spending better

- using up gift cards

- not buying new stuff

- selling used school curriculum

- doing a pantry challenge to offset grocery spending

- scrolling through my Amazon purchases to see if there were purchases I made on a whim that I don’t actually love

5. Revisit your budget frequently.

Every month you need to write a new zero based budget. That was the thing I didn’t understand as a young bride. Every month is different. Your family has different needs, and you need to adjust accordingly.

When you’re just starting out — or getting back in the swing of things — I recommend revisiting the budget and retallying expenses on a weekly or bi-weekly basis. The more it’s in your face, the more diligent you’ll be.

You will get better at budgeting the more you do it. I promise.

More Good Ideas for Budgeting

What do you think?

I’d be honored if you chimed in the comments section. What do you think?

This post was originally published on August 21, 2014. It has been updated for content and clarity.

This post is as sound today as it was a decade ago.

Awww, thank you!

I remember you used to have some free budgeting printables on your site—do you still have those? I looked around but couldnt find them.

Are you talking about these? http://lifeasmom.com/2012/10/keep-track-of-financial-stats-and-monthly-costs.html

I have a spreadsheet with a tab for every month. We track what comes in and what goes out every month down to the penny! We are paying down a large student loan and everything extra every month goes directly to that loan. I will make 2-3 payments a month on it as soon as extra cash appears in our budget. I know we are lucky to have the funds to pay it down, but sometimes I hate watching our money that closely every month. Once the loan is gone, we are going to have a couple of months of “fun money” and not watching the budget then tighten down again and start attacking our mortgage!

Keep on keeping on! You can do it!

Check out YNAB (You Need A Budget). It is a budgeting program that has completely changed my financial life for the better. It does all the things you talked about above in a practical user-friendly way. I use it, and 3 of my adult children also use it. I use it strictly on my home computer, but my kids all also access it from their smart phones, enabling them to enter transactions literally at the cash register as they check out.

I completely agree Mary. My husband and I are die-hard YNAB users. It completely changed our financial life as well. The $60 investments pays for itself easily. We love the easy accessibility on our smart phones, the flexibility, and the user friendliness.

Thanks for the tip. Is it a yearly fee?

Sorry, I just came across your question – it got lost in my email. YNAB costs $60, one-time-only fee, then it is yours forever.

YNAB has basically saved my marriage. No lie. We finally found something we could both understand and it made sense with our commission based income. We have to live on last mo THS income because we have no idea what we will make this month. It just finally made sense instead of trying to predict the future!!